Praseodymium-Neodymium Recycling Technologies: Current Status and Economic Viability Analysis

Abstract:

As global demand for NdFeB permanent magnets accelerates across electric vehicles, wind energy, and robotics sectors, praseodymium-neodymium recycling from end-of-life magnets and manufacturing scrap has emerged as a strategic pillar of rare earth supply security. This white paper provides a comprehensive analysis of current Pr-Nd recycling technologies, their industrial deployment status, and quantitative economic assessment. Drawing on the latest peer-reviewed research, patent filings, and market data up to May 2026, this report examines hydrometallurgical, pyrometallurgical, and emerging recycling approaches alongside the financial performance of major industry participants.

1. Introduction

Rare earth permanent magnets, particularly neodymium-iron-boron magnets, are critical components in clean energy technologies and advanced manufacturing. However, primary rare earth mining faces mounting constraints: declining ore grades, stringent environmental regulations, and concentrated supply chains. China‘s rare earth reserves have declined from 74% of the global total in the 1970s to 33% by 2022.

Recycling of Pr-Nd from secondary resources—particularly NdFeB manufacturing scrap and end-of-life magnets—offers a strategically vital alternative. NdFeB waste contains rare earth concentrations of approximately 30%, far exceeding the 4% typical of primary ores. Global end-of-life NdFeB magnet volumes from wind turbines alone are projected to reach 5,000 tonnes by 2034.

Global demand for rare earth permanent magnets is projected to grow 69% by 2036, exceeding 332,000 tonnes annually. Magnets can contain up to 32% (by weight) of high-value elements including neodymium, praseodymium, dysprosium, and terbium, compared to high-grade ore deposits which typically contain only about 12%. This concentration differential forms the fundamental economic rationale for recycling.

2. Technology Landscape

2.1 Hydrometallurgical Routes

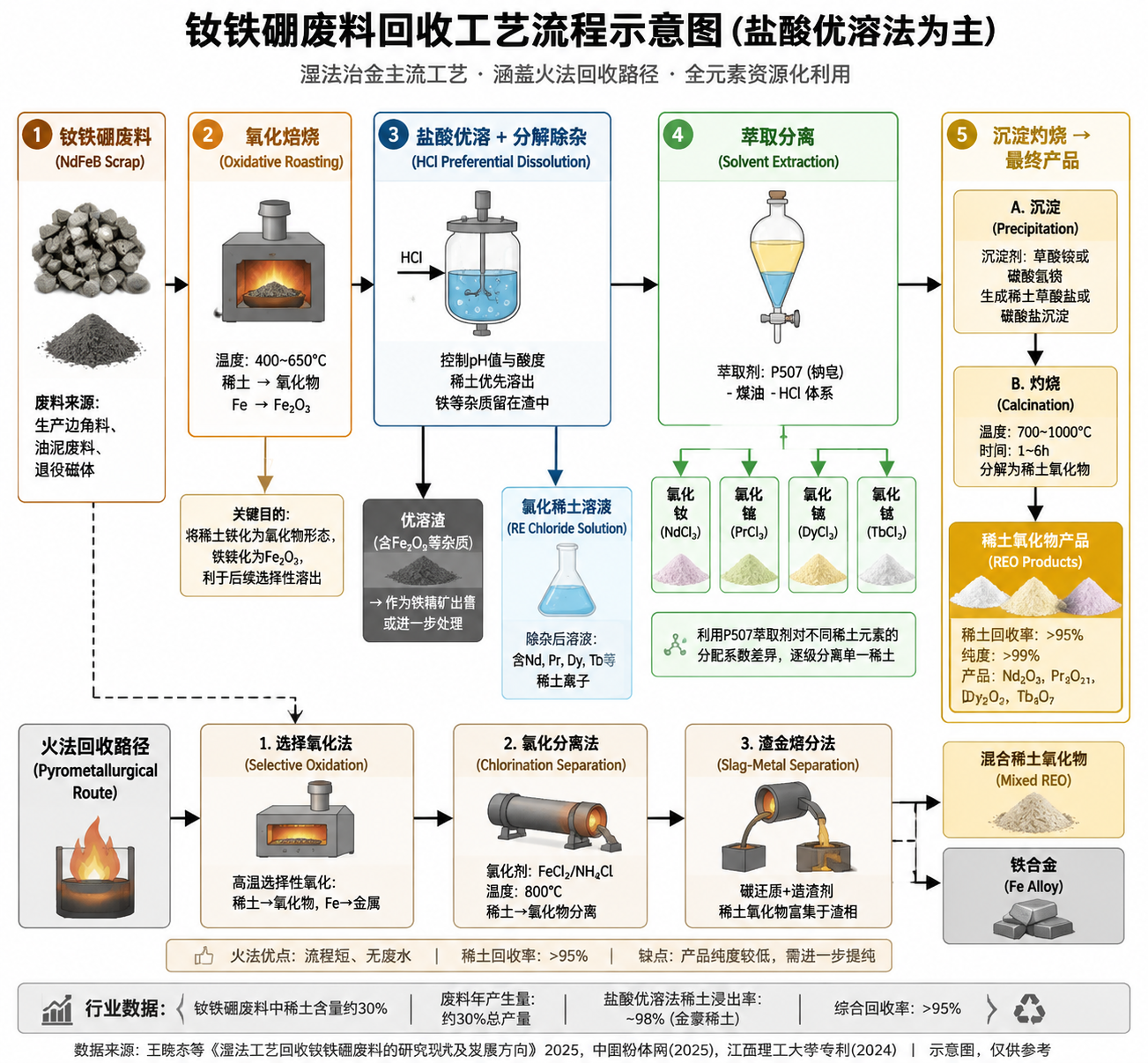

Hydrometallurgical processing remains the most widely commercialized technology for Pr-Nd recovery from NdFeB waste. The typical process involves acid dissolution of rare earth elements from waste materials, followed by solvent extraction or ion exchange for separation and purification. These methods offer high recovery rates and good selectivity, making them particularly advantageous for processing complex waste streams.

A unified framework for rare earth recycling published in April 2026 by the Chinese Academy of Sciences distinguishes between pre-separation (conversion and conditioning of complex matrices) and downstream separation and refining. The framework highlights intrinsic trade-offs that govern recycling viability: selectivity versus robustness, chemical intensity versus scalability, and recovery efficiency versus environmental impact.

Hydrochloric Acid Selective Dissolution: Baogang Group‘s Jinmeng Rare Earth facility has developed an optimized HCl selective dissolution process achieving rare earth leaching efficiency of 98%. The process involves oxidative roasting of NdFeB waste, followed by precisely controlled acid dissolution that selectively leaches trivalent rare earths into solution while leaving iron in the residue. The resulting rare earth chloride solution undergoes solvent extraction separation and oxalic acid precipitation to yield high-purity mixed or individual rare earth oxides.

Full-Element Recovery: A 2025 patent by Grirem Advanced Materials and partners described an integrated process combining organic solvent extraction with dual-resin adsorption-desorption separation, enabling simultaneous recovery of rare earth elements and valuable metals from NdFeB waste leachates. This approach addresses the challenge of impurity metal interference while achieving high-value utilization.

2.2 Pyrometallurgical Routes

Pyrometallurgical recycling, leveraging high-temperature reactions to separate rare earths from iron, is gaining attention due to its short process flows, scalability, and environmental advantages.

Selective Chlorination: Using FeCl₂ as the chlorinating agent and activated carbon as reductant at 1073K for 12 hours, this method achieves rare earth recovery of 95.9% with product purity of 99.2%. The process generates no toxic pollutants or wastewater in principle. Rare earth chlorides can be converted to corresponding oxides through thermal hydrolysis, with the HCl generated being recyclable for iron chlorination.

Low-Temperature Chlorination-Water Leaching: A patent granted in November 2025 describes a process using NH₄Cl for chlorination roasting at 200–450°C—significantly lower than conventional chlorination temperatures. The process exploits the differential reactivity of rare earths versus iron toward chlorine, selectively converting rare earths to water-soluble chlorides while leaving iron unreacted. Subsequent water leaching, iron removal, oxalic acid precipitation, and calcination yield mixed rare earth oxides.

2.3 Emerging Technologies

Biohydrometallurgy: Baogang Group established a rare earth bio-metallurgy joint research base in June 2025, pursuing microbial synthesis approaches for efficient leaching, enrichment, and separation of rare earths from tailings and urban waste streams.

Hydrogen Decrepitation: This short-loop recycling route uses hydrogen to fracture NdFeB magnets along grain boundaries, enabling direct regeneration into new magnets. The process has a significantly lower global warming potential compared to elemental recovery, but faces challenges including stringent feedstock specifications and numerous variables affecting final magnetic properties.

Electrochemical Methods: Research into electrodeposition and electrodialysis for rare earth recovery is ongoing, offering high selectivity with reduced chemical consumption, though these remain at laboratory scale.

3. Industrial Deployment

3.1 Capacity Expansion

China‘s rare earth waste recycling sector experienced substantial capacity growth in 2025, with total oxide-equivalent capacity expanding from under 40,000 tonnes to over 60,000 tonnes, concentrated in Q2-Q3. In 2026, end-of-life waste contribution is projected to increase from 25% to 30% of total feedstock, with the ratio of new manufacturing scrap to end-of-life waste shifting from 3:1 to 3:2.

3.2 Major Projects

Baogang Group Jinmeng Rare Earth: A 4,000-tonne/year NdFeB waste recycling automated production line commenced trial operations in January 2026. The facility processes approximately 20,000 tonnes of NdFeB waste annually, producing approximately 4,000 tonnes of rare earth oxides. The project fills a critical industrial gap in Inner Mongolia‘s rare earth waste processing sector.

Huahong Technology: As China‘s leading rare earth recycling enterprise, Huahong achieved annual recycled rare earth oxide production capacity exceeding 12,000 tonnes following the commissioning of Phase II expansion projects at Xintai Technology and Wanhong High-Tech. 2026 capacity has potential for 30% further growth. In 2025, the company sold 9,166 tonnes of rare earth oxides, a 57.11% year-on-year increase.

Ganzhou Huazhuo: With designed capacity of 68,000 tonnes/year of mixed rare earth oxide feedstock (approximately 17,000 tonnes REO), this facility accounts for 45% of national recycling feedstock capacity, generating over RMB 13 billion in annual revenue with fewer than 50 frontline workers.

3.3 Industry Recovery Rates

China‘s rare earth recovery rates have exceeded 90%, significantly surpassing the approximately 85% average of the United States and Japan.

4. Economic Viability Analysis

4.1 Market Fundamentals

Pr-Nd oxide prices experienced a dramatic rally, rising from RMB 345,000/tonne in March 2024 to RMB 870,000/tonne in March 2026—an increase exceeding 150%. As of May 25, 2026, Pr-Nd oxide averaged RMB 683,100/tonne, with Pr-Nd metal at RMB 839,500/tonne.

The global rare earth recycling market is valued at approximately USD 0.68 billion in 2026, projected to reach USD 1.66 billion by 2034 at a CAGR of 11.7%. The electronics rare earth recycling segment alone accounts for USD 7.40 billion in 2026, projected to reach USD 22.60 billion by 2034 at a CAGR of 15%.

4.2 Corporate Financial Performance

| Metric | Huahong Technology FY2025 | YoY Change |

| Rare Earth Recycling Revenue | RMB 4.081 Bn | +64.17% |

| Rare Earth Recycling Gross Margin | 10.71% | +8.71 PCT |

| Rare Earth Oxide Sales Volume | 9,166 tonnes | +57.11% |

| Net Profit | RMB 204 Mn | Turned profitable |

| Q1 2026 Revenue | RMB 2.512 Bn | +74.93% |

| Q1 2026 Net Profit | RMB 216 Mn | +595.21% |

Shenghe Resources reported FY2025 revenue of RMB 14.991 billion (+31.83% YoY) and net profit of RMB 839 million (+304.94% YoY).

4.3 Profit Sensitivity

Brokerage analysis indicates that for every RMB 100,000/tonne increase in Pr-Nd oxide average price, Huahong Technology‘s quarterly net profit increases by approximately RMB 80 million. Conversely, every RMB 50,000/tonne increase in NdFeB scrap procurement cost reduces quarterly net profit by approximately RMB 45 million.

4.4 Lifecycle Cost Comparison

Recycling-based neodymium metal production achieves a cost of USD 3.98/kg, compared to USD 8.55/kg for primary mining—a 53% reduction. Recycling routes also reduce the environmental impact of NdFeB magnet production by up to 65% across eight of eleven assessed environmental impact categories.

4.5 Structural Cost Advantages

The economic competitiveness of Pr-Nd recycling rests on three structural advantages: feedstock concentration (~30% REE in waste vs. ~4% in ore), elimination of mining and beneficiation stages, and exemption from mining quotas and resource taxes. These factors combine to produce substantially lower production costs compared to primary extraction routes.

5. Policy Framework and Market Drivers

In September 2025, eight Chinese ministries jointly issued the Nonferrous Metals Industry Stable Growth Work Plan (2025–2026), explicitly supporting the establishment of renewable resource recovery bases and strengthening comprehensive utilization of nonferrous metal waste, including spent power batteries and photovoltaic modules. The Plan also emphasized breakthroughs in high-end rare earth new materials.

2025 saw further tightening of rare earth regulations: import ores and by-product ores were brought under total volume control for the first time; export controls were imposed on medium and heavy rare earth metals, alloys, oxides, and compounds; and NdFeB magnet manufacturing core equipment was placed under export control.

6. Challenges and Risk Factors

Despite strong economic returns during price upcycles, the recycling sector faces structural vulnerabilities:

- Price volatility: When primary rare earth prices decline due to oversupply or illegal mining, recycling economic viability can collapse rapidly.

- Technological complexity: Sophisticated separation processes required for individual REE extraction consume significant energy and reagents while generating secondary waste streams.

- Feedstock dispersion: End-of-life magnets are widely dispersed across product types and geographies, challenging cost-effective collection and pre-processing. Comprehensive reviews emphasize the urgent need for automated disassembly equipment and selective recovery technologies alongside Extended Producer Responsibility schemes.

- Illegal mining competition: During price spikes, unauthorized primary smelters operating under the guise of “waste recycling” rapidly expand production, quickly depressing market prices and undermining legitimate recyclers‘ investment returns.

7. Outlook and Strategic Implications

Pr-Nd recycling is transitioning from a supplementary activity to a core pillar of rare earth supply security. The share of recycled material in total Pr-Nd supply is projected to increase from approximately 20% to over 30% within the next decade.

Key development trajectories include: expansion toward full-element recovery maximizing value extraction from waste; advancement of short-loop, low-carbon regeneration technologies; establishment of comprehensive end-of-life product collection infrastructure; and enhanced integration of recycling operations with magnet manufacturing for closed-loop supply chains.

With the global rare earth recycling market projected to more than double by 2034, and electronics recycling growing at 15% CAGR, the strategic and economic significance of Pr-Nd recycling will continue to accelerate.